We don't just talk about our performance. We prove it to you.We aim higher than just resetting the standards within the forex industry – we also deliver the highest levels of transparency to all our clients. The statistics below show exactly why we're so proud of our trading conditions, which include some of the best spreads in the business.

Forex news for Asia trading on Friday 13 August 2021

It was a small range session for major FX here in Asia on the 13th. The USD weakened just slightly with a marginal gain for EUR, AUD, NZD, GBP. Yen, CHF and CAD are probably characterised better as unchanged but there isn’t much in it.

The inflation debate is raging in financial markets and we can see just how sensitive price action is after today’s US CPI data. The numbers were generally in line with forecasts and yet the dollar is down sharply across the board.

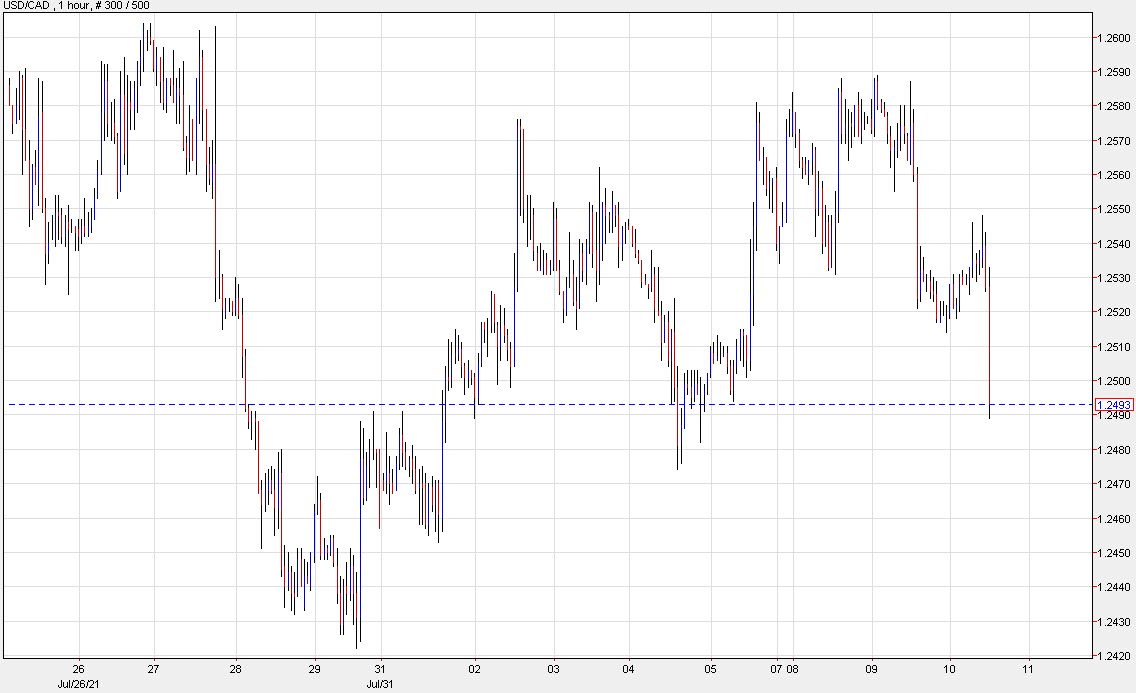

One example is USD/CAD, which is down nearly 40 pips and through 1.25 to the lowest in four days.

I’m surprised by the size of these moves but it speaks to the taper debate (Sept vs Dec) along with the pace of the taper once it starts. Ultimately though, it relates back to interest rates and if inflation comes down on its own, then there’s no need for the Fed to ever get above something like 1% on fed funds.

What’s interesting to me here is how substantial this move has been on an ‘in line’ print on CPI. That suggests that dollar longs are crowded, something Goldman Sachs recently warned about.

Forex news for North American trading on August 6, 2021

The awaited jobs report was released today at 8:30 AM ET, and it did not disappoint. The net change in nonfarm payroll jobs was 943K. That was above the 870K estimate. Moreover, the June report was revised higher by 88K to 938K, and the May report was also revised higher by 31K to 614K (from 583K).

Overall, with revisions, the US added 1.062M jobs which is good news for the economy.

Making the report even more impressive was that the unemployment rate tumbled to 5.4% from 5.9% last month. The underemployment rate fell to 9.2% from 9.8%. Hourly earnings rose by 0.4%, and the year on year measure is now up 4.0% year on year versus 3.9% estimate (and 3.4% last month).

Leisure and hospitality led with a gains with 380K jobs added.

Government added 240K

Professional business services, +60K

education and health services, +87K

transportation and warehousing, +49.7K

The one cautionary tone is that the local government education category (part of Government) is out of sync with the seasonal adjustments due to Covid. It showed a oversized 220K increase in jobs and may have a “give back” in coming months. Nevertheless, the report was still very solid.

As a result, traders will now be looking for Fed comments as the market prepares for a taper that may/should be sooner than expected.

Fed’s Clarida said this week that he could see a December taper . Fed’s Wallers, Bullard and Kaplan would rather start the taper sooner rather than later so the Fed could have flexibility to tighten interest rates in 2022 if needed. Next week, the market will hear from Fed’s Bostic, Evans, George and Barkin are all expected to speak next week. I would imagine, it will be hard to keep Fed’s Bullard from an interview at some point (he is not shy especially if he is right and he has been one of the more hawkish Fed officials and will be voting in 2022).

Goldman Sachs increased their chances for a November taper to 25% and December 55%. The Fed Chairs Jackson Hole speech (the event takes place from August 26 to August 28) becomes days to circle on the calendar for taper clues.

The reaction in the markets saw:

The USD move higher

Flow in stocks into the Dow cyclicals and out of technology (i.e. Nasdaq)

Higher US rates

Lower gold.

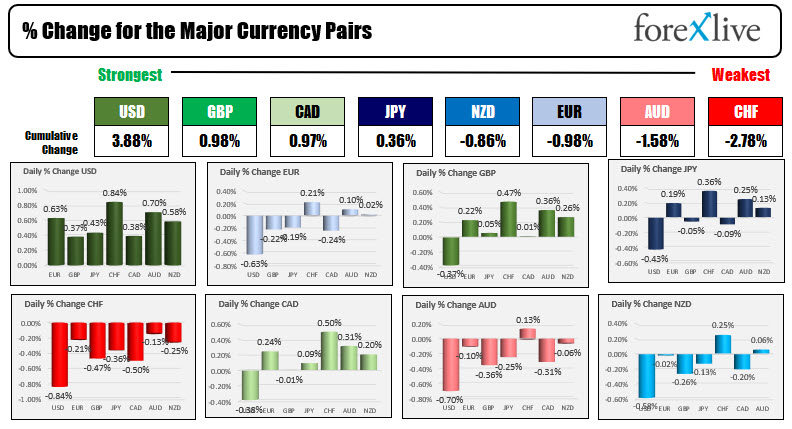

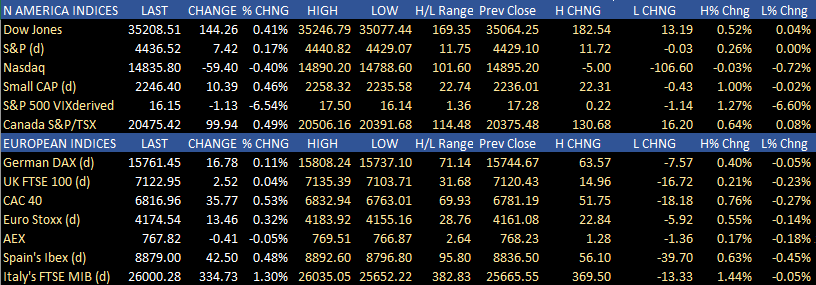

Looking the strongest to weakest in the forex market, the USD is ending the day as the run-away strongest of the major currencies. The CHF and the AUD were the weakest.

In the US stocks, the Dow and S&P indices both closed at record levels with the Dow leading with a gain of 0.41%. Leading the charge today were financials which rose 2.01%. Materials (+1.47%) and Energy (+0.94%) were also winners today. Discretionary (-0.73%), real estate (-0.25%) and technology (-0.12%) were the laggards.

The Nasdaq index light with a -0.4% decline after closing at a record level on Thursday. Despite the decline today, the NASDAQ index led the way with a 1.0% gain for the week.

In the European market today, the major indices all closed higher but off their highs levels. The France’s CAC rose by 0.53% and closed at its highest level since 2000. It is only 100 points or so from its all-time record high.

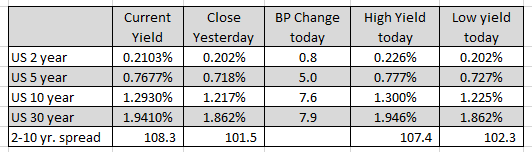

In the US debt market, yields this week trade as low as 1.127% in the benchmark 10 year yield. The yield is going out the week at 1.293% up nearly 16 basic point from the weeks low. Next week will be a key test for the global demand of US debt, as the U.S. Treasury will auction off:

$58 billion of 3 year notes on Tuesday,

$41 billion of 10 year notes on Wednesday, and

$27 billion of 30 year bonds on Thursday.

In other markets today:

Spot Gold tumbled $41.50 or -2.3% to $1762.76

Spot Silver fell $0.83 or -3.33% to $24.29

WTI crude oil futures felt $-1.14 or -1.66% at $67.97. For the week, crude oil fell over 7% from Friday’s closing levels

The price of bitcoin rose $1838 to $42,733.48. The price is trading at the highest level since May 19, 2021. The 200 day moving average going into the weekend is currently at $44,822. Will traders squeeze the price toward that key MA level? I would not be surprised.

Wishing you all a great and healthy weekend. Thank you for your support this week.